Monday, October 21, 2024

Wednesday, September 18, 2024

Sumatran Squall, 17 Sept 2024

A report on the Sumatra Squall that struck Singapore on 17 Sept.

CNA Explains: What is a Sumatra squall and how did it bring a sudden storm to Singapore?

What are the characteristics of a Sumatra squall? How often does it occur and how bad can it get? CNA speaks to weather experts.

Lessons from Russo-Ukraine War

Video: Singapore is studying Ukraine conflict very closely: Ng Eng Hen (CNA)

Ukraine is “the most modern fought war in recent times”.

Tuesday, September 17, 2024

Pope Francis commends Singapore's policies supporting the vulnerable, hopes for special attention to poor and elderly

Pope Francis also highlighted the risk of focusing solely on pragmatism or "placing merit above all things", consequently excluding the marginalised from benefiting from progress.

Ang Hwee Min

12 Sep 2024

SINGAPORE: Pope Francis has commended Singapore's policies to support the most vulnerable, adding that he hopes special attention will be paid to the poor and the elderly.

|

| Pope Francis and Singapore President Tharman Shanmugaratnam at the pope’s state address on Sep 12, 2024. (Photo: CNA/Syamil Sapari) |

Ang Hwee Min

12 Sep 2024

SINGAPORE: Pope Francis has commended Singapore's policies to support the most vulnerable, adding that he hopes special attention will be paid to the poor and the elderly.

Friday, September 13, 2024

New "United Front"? Chinese Agents in South East Asia?

Firstpost is an India-based, obviously biased, anti-Chinese, news channel. So they would highlight or feature any news item that would put China in a bad light. But they do also cover the news about China, like this story about Linda Sun and Alice Guo.

Monday, August 12, 2024

Singapore looks to build first-of-its-kind renewable energy farm in waters around Raffles Lighthouse

|

| Raffles Lighthouse on Pulau Satumu, the southernmost islet in Singapore waters. (Photo: Chew Hui Min) |

The energy generated could be used to charge electric harbour craft, in line with upcoming requirements to decarbonise the maritime industry.

Jeraldine Yap

Louisa Tang

09 Aug 2024

SINGAPORE: A renewable energy farm could be built in the waters around Raffles Lighthouse, with a feasibility study expected to begin in the fourth quarter of this year.

The Maritime and Port Authority of Singapore (MPA) told CNA that it has earmarked 30ha around the island and is looking into installing solar panels above the sea surface and tidal turbines underwater.

Observers said it would be the first facility in Singapore to combine harnessing energy from the sun as well as tides on a large scale.

Saturday, August 10, 2024

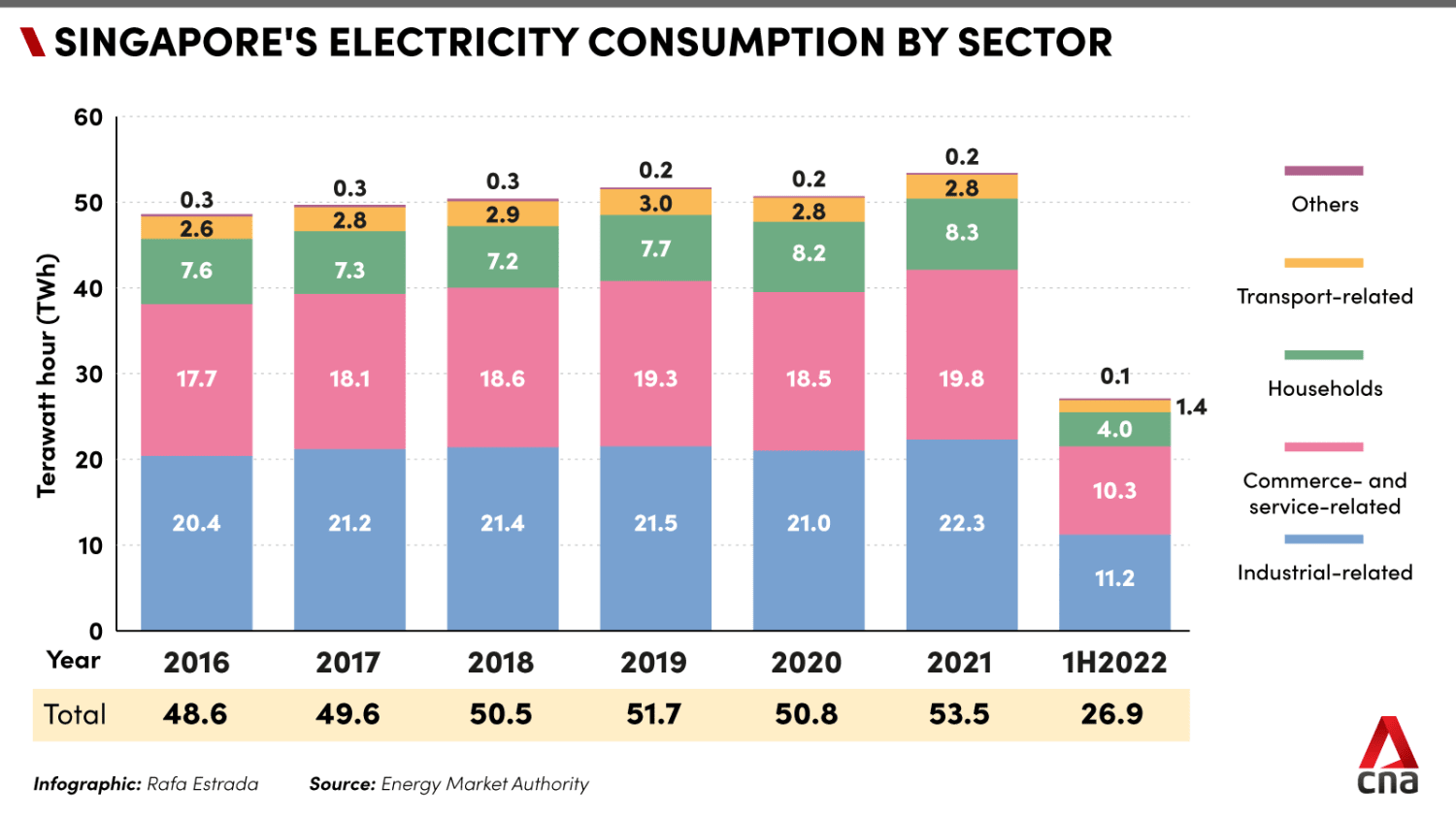

CNA Explains: Singapore's energy sources and the future of its electricity supply

Why does Singapore need to import its electricity? Why can't it just rely on solar power?

Gabrielle Andres

SINGAPORE: Where Singapore gets its electricity from has been in the headlines in recent months, with the announcement that the country will import electricity from Malaysia and the opening of the largest energy storage system in Southeast Asia on Jurong Island.

Last Monday (Jan 30), it was announced that Singapore will import 100 megawatts (MW) of electricity from Malaysia as part of a two-year trial, under a joint agreement between YTL PowerSeraya and TNB Genco.

Gabrielle Andres

07 Feb 2023

SINGAPORE: Where Singapore gets its electricity from has been in the headlines in recent months, with the announcement that the country will import electricity from Malaysia and the opening of the largest energy storage system in Southeast Asia on Jurong Island.

Last Monday (Jan 30), it was announced that Singapore will import 100 megawatts (MW) of electricity from Malaysia as part of a two-year trial, under a joint agreement between YTL PowerSeraya and TNB Genco.

Subscribe to:

Posts (Atom)